We Calculated How Much the App Store Payout Delay Actually Costs

Your app generated £84,000 in revenue last month. Your bank account shows £11,400. The business isn't losing money — it's waiting for it. Between the moment a user taps "Subscribe" and the moment that revenue hits your bank account, somewhere between 33 and 63 days disappear into Apple's and Google's processing pipelines.

Everyone in the mobile app industry talks about growth: downloads, ARPU, LTV, ROAS. Almost nobody talks about the cost of waiting for money you've already earned. That cost is real, it compounds every month, and for most studios, it's far larger than they assume.

We built a model to calculate the actual financial impact of payout delays across three studio sizes. The numbers surprised us — and they'll probably surprise you.

How the delay actually works

Apple and Google don't pay developers on a standard monthly calendar. Understanding the mechanics matters, because the delay is longer and more variable than most founders realise.

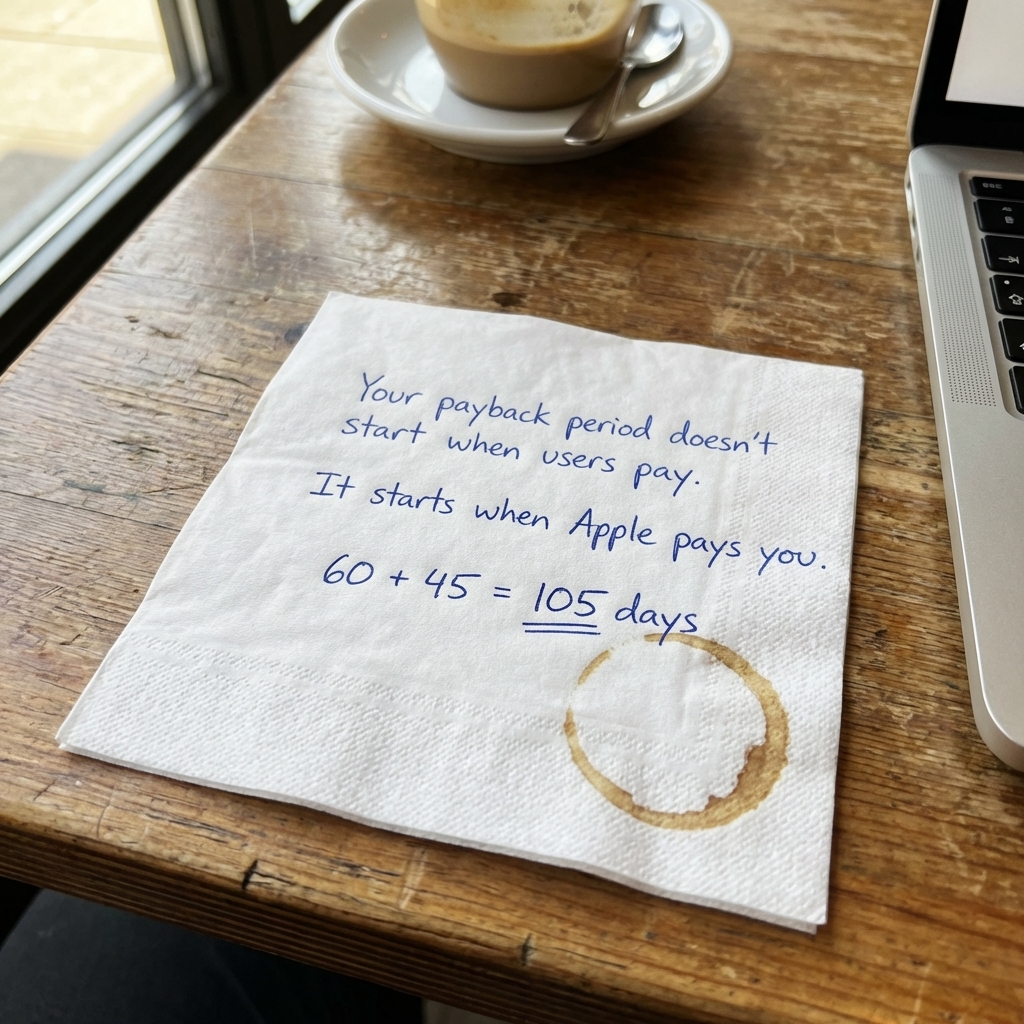

Apple App Store uses a 4-5-4 fiscal calendar — not standard calendar months. Each quarter is divided into three earning periods of alternating 4-week and 5-week lengths. When an earning period closes, Apple begins a processing window of approximately 33 days before releasing funds.

Here's what that looks like in practice. A user subscribes to your app on 1 January. That transaction falls into an earning period that closes around 31 January. Apple then takes roughly 33 days to process, putting your payout around 5 March. That's 63 days from the transaction to your bank account. If the same user subscribed on 20 January — still within the same earning period — they'd wait 44 days. The delay depends entirely on where within the earning period the transaction occurs.

Google Play operates on standard calendar months, which is simpler but still slow. Earnings from January become payable in February, with actual disbursement typically arriving between the 15th and 30th of the following month. Real-world delays range from 15 to 45 days depending on your bank, country, and payment method.

Neither platform designed this to penalise developers. The delay exists for processing refunds, handling chargebacks, and managing fraud detection across millions of transactions. But the financial impact on your studio is the same regardless of the reason.

See all upcoming payout dates on our Payment Calendar.

The math: three studio profiles

Below are models for three studio sizes. Every formula is shown so you can substitute your own numbers. We use a 45-day average delay — conservative for Apple, generous for Google — as the baseline.

The core formula for frozen capital:

Frozen Capital = Monthly Store Payouts × (Average Delay Days ÷ 30)

This represents the amount of earned revenue that's perpetually locked in the payout pipeline. It's not a one-time freeze — this amount is always unavailable, rolling forward month after month.

Profile A: Indie Studio

| Metric | Value |

|---|---|

| Monthly store payouts | £25,000 |

| Average delay | 45 days |

| Frozen capital (at any given time) | £25,000 × 1.5 = £37,500 |

Direct cost — credit card bridging. Many indie founders bridge the gap with business credit cards. At a typical UK business card APR of 24%, carrying £37,500 costs:

£37,500 × 24% = £9,000 per year (£750/month)

That's 3% of annual gross revenue spent on interest — just to access money you've already earned.

Opportunity cost — UA deployment. If that £37,500 were available and deployed into user acquisition at a 2x ROAS over 180 days (a conservative benchmark for well-optimised campaigns), one capital cycle looks like this:

£37,500 spent on UA → £75,000 revenue within 180 days → £37,500 net return

With two deployment cycles per year, the annual opportunity cost reaches £75,000 in revenue you never captured — three full months of payouts.

Combined annual impact: £9,000 direct cost + £75,000 in missed revenue = £84,000

Profile B: Mid-Size Studio

| Metric | Value |

|---|---|

| Monthly store payouts | £80,000 |

| Average delay | 45 days |

| Frozen capital (at any given time) | £80,000 × 1.5 = £120,000 |

Direct cost — credit card bridging. At 24% APR:

£120,000 × 24% = £28,800 per year (£2,400/month)

In practice, most business credit cards cap at £50,000–£100,000. A studio at this level likely can't even bridge the full gap with cards — they're forced to ration UA spend or delay vendor payments instead.

Opportunity cost — UA deployment. At 2x ROAS D180, two cycles per year:

£120,000 × 2 cycles × (2x – 1x) = £240,000 in unrealised annual revenue

That's the equivalent of hiring three senior engineers or funding a full quarter's UA campaign. Every year.

Combined annual impact: £28,800 direct + £240,000 opportunity = £268,800

Profile C: Scaling Studio

| Metric | Value |

|---|---|

| Monthly store payouts | £300,000 |

| Average delay | 45 days |

| Frozen capital (at any given time) | £300,000 × 1.5 = £450,000 |

Direct cost. Credit cards are impractical at this scale. A business overdraft facility at 10% interest (if available, which requires collateral and board-level approval):

£450,000 × 10% = £45,000 per year

Opportunity cost — UA deployment. At 2x ROAS D180:

£450,000 × 2 cycles × (2x – 1x) = £900,000 in unrealised annual revenue

At this level, the payout delay isn't a nuisance — it's the difference between hitting growth milestones and missing them. £450,000 perpetually locked in the pipeline means delayed hires, abandoned UA windows, and slower international expansion.

Combined annual impact: £45,000 direct + £900,000 opportunity = £945,000

Your own calculation

Plug in your numbers:

- Frozen capital = Your monthly store payouts × 1.5

- Direct cost = Frozen capital × your financing rate (credit card APR, overdraft rate, etc.)

- Opportunity cost = Frozen capital × expected ROAS × number of capital cycles per year

- Total annual impact = Direct cost + Opportunity cost

Even if you use conservative ROAS estimates — say 1.5x instead of 2x — the numbers are substantial. For Profile B at 1.5x ROAS, the opportunity cost alone is still £120,000 per year.

The compound problem: faster growth = bigger gap

Here's the part that catches studios off guard. The payout delay doesn't just cost a fixed amount — it scales with your success.

Consider Profile B growing at 15% month-over-month, a strong but not unusual trajectory for a studio that's found product-market fit:

| Month | Monthly Revenue | Monthly Costs | Frozen Capital |

|---|---|---|---|

| 1 | £80,000 | £64,000 | £120,000 |

| 3 | £105,800 | £84,600 | £158,700 |

| 6 | £161,000 | £128,800 | £241,500 |

| 9 | £245,000 | £196,000 | £367,500 |

| 12 | £373,000 | £298,400 | £559,500 |

Revenue quintupled. Frozen capital quintupled with it — from £120,000 to nearly £560,000. But here's the crucial detail: costs (payroll, UA, servers, tools) scale immediately with growth, while revenue arrives 45 days later.

By month 9, this studio needs £196,000 in cash every month for operating costs. Its frozen capital is £367,500 — nearly two months of expenses trapped in the pipeline. The faster the studio grows, the wider the gap between what it needs and what it has.

This is why studios that look "successful" on paper sometimes face genuine cash crises. Their P&L is healthy. Their bank balance tells a different story.

What studios actually do about it

The industry has developed several approaches to this problem, each with trade-offs worth understanding.

Credit cards and overdrafts. The most common stopgap. Fast to set up, but expensive (20–30% APR for cards, 8–12% for overdrafts) and limited by credit ceilings. Works for small gaps; collapses at scale.

Revenue-based financing and factoring. A category of providers that advance capital against confirmed app store revenue. Models vary widely — some require rerouting your payouts to the provider's account, others use different structures. The key questions: what's the real all-in cost, and who controls the money?

Equity and venture capital. Solves the cash problem entirely, but introduces dilution and takes 3–6 months to close. Not a realistic fix for a cash gap that hits every 30 days.

Waiting it out. The default choice for many studios, and the most expensive one — because the opportunity cost of idle capital compounds silently month after month.

Each approach carries different risk profiles and cost structures. The right choice depends on your studio's size, growth rate, and how much control you need over your cash flow.

See your exact numbers

A studio earning £80,000 per month carries roughly £120,000 in permanently frozen capital, losing between £28,800 (direct financing costs) and £268,800 (including missed growth opportunities) annually. For a £300,000/month studio, the figure approaches £1 million.

These aren't hypothetical losses — they're the compounding cost of a 45-day structural delay in a market where global app revenue exceeded $171 billion in 2024 and UA windows measured in days determine quarterly outcomes.

Your studio's exact number depends on your revenue mix, growth rate, and current financing costs. We built the App Revenue Intelligence Report to calculate it: enter your App Store and Google Play payout data, and get a personalised breakdown of your frozen capital, direct costs, and opportunity cost.

At Amps33, we built this calculator because the first step to fixing a problem is knowing its actual cost. See your numbers →